The Future of Pharmacy: What the MHE 2026 Pharmacy Survey Signals for the Year Ahead

- Apr 13

- 5 min read

By Marina Crouse, Peter Wehrwein, Managing Editor | Original Article

Key Takeaways

Escalating specialty drug expenditures are forcing tighter utilization management while preserving equitable access, outcomes, and quality metrics across formularies and integrated delivery networks.

GLP-1 uptake is stressing pharmacy and medical benefits, while unclear coverage, contracting, and policy trajectories creating operational complexity for plans, providers, and employers.

Divergent views on most-favored-nation pricing reflect trade-offs between near-term unit price reductions and downstream impacts on innovation incentives, market dynamics, and patient access.

Strategic anxiety persists regarding sustained drug price inflation and the possibility that U.S. policy shifts could weaken global leadership in pharmaceutical R&D and commercialization.

The 2026 MHE Pharmacy Survey asked questions about most-favored nation drug pricing, PBM reform and HHS Secretary Robert F. Kennedy Jr.'s vaccine policies. Respondents rated direct-to-consumer drug sales by drugmaker as the most important development in the pharmaceutical sector this year.

As the role of pharmaceuticals continues to expand across the healthcare ecosystem, stakeholders are navigating a landscape increasingly shaped by rising specialty drug costs, evolving policy pressures and ongoing scrutiny of pricing and reimbursement models. To better understand these dynamics, Managed Healthcare Executive conducted its annual Pharmacy survey, capturing perspectives from payers, pharmacy leaders, health systems, academic institutions, government and pharmacy benefit managers (PBMs). To help contextualize what these changes mean for the future of care delivery and cost management, we invited three experts to share their thoughts.

The findings offer a snapshot of the forces driving pharmacy today — from cost and utilization trends to policy and market shifts.

Here are the commentators on our survey.

|  |  |

Vice President and Strategic Business Advisor, Gilroy Kernan & Gilroy | Executive Vice President of Clinical Pharmacy, IPD Analytics LLC | Vice President of the Market Access Center of Excellence, IQVIA |

Managed Care Advisor, Managed Care Resource Alliance | MHE Editorial Advisory Board Member | MHE Editorial Advisory Board Member |

Four Takeaways

Pharmacy stakeholders are balancing increasing cost pressures with the need to maintain patient access and quality of care.

The glucagon-like peptide 1 (GLP-1) drugs present cost challenges and policy uncertainty across settings.

The Trump administration's most-favored-nation drug pricing policies get mixed reviews.

Chief concerns about the future of pharmaceutical sector include the cost and price of drug and the U.S. losing its competitive advantage.

MHE 2026 Pharmacy Survey Results

“Two major findings stood out to me: I was surprised to see that Biologics vs. Biosimilars was not listed. Biologics are made from living cells whereas biosimilars are highly similar versions of an approved biologic with no clinically meaningful differences in safety, purity, or potency. While biosimilars are not identical to biologics due to biologic complexity, they are rigorously compared to the reference product and cost 30% to 75% less than biologics and, in some cases, even 90% less. Many top performing employers examine these opportunities frequently, as hundreds of thousands of dollars, for just a few of these drugs, can be at risk annually.

“Also, emphasis on manufacturer assistance programs (and other similar programs), which are sponsored by pharmaceutical companies to provide free or low-cost medications to individuals who are uninsured, underinsured or meet specific financial hardship criteria. These programs help reduce out-of-pocket costs for plan participants and sponsors and are usually accessed directly through the manufacturer or an authorized medicine assistance tool.”

—Andrew F. Biernat, GBDS, CWCA

“From a therapeutic area perspective, the responses clearly show that obesity and the GLP-1s remain front and center in 2026. That is not necessarily new, but that the attention remains focused on this area by more than half of all respondents shows how widespread utilization is. That obesity is neck and neck with cancer as cost drivers over the next three years shows just how big the class is expected to get.”

—Luke Greenwalt, MBA

“Survey respondents did not see MFN as impactful. MFN may not be implemented long-term in the form we envision today but I do see this initial push to change the price paradigm in the U.S. as industry-altering. MFN discussions and the price equalization movement will ultimately lead to a world where U.S. prices are more in line with other developed nations.”

—Jeff Casberg, RPh, M.S

“Short term (1-year outlook): Policy uncertainty and legal challenges could likely limit full implementation. Still, the signal alone could pressure manufacturers to moderate price increases, especially for high-cost drugs (e.g., Part B/administered therapies). Providers may see reimbursement volatility if payment benchmarks shift faster than acquisition costs, creating margin compression. PBMs and plans may gain short-term leverage in negotiations but face formulary disruption risks.

“Medium term (3-year outlook): If sustained, MFN could structurally lower U.S. prices for select drugs but drive strategic manufacturer behavior: tighter launch sequencing, reduced discounts abroad and potential narrowing of U.S. availability for lower-margin therapies. Providers (especially hospital outpatient departments) could face persistent reimbursement gaps. Payers/employers may benefit from lower unit costs but contend with utilization management complexity. Patients could see lower cost-sharing on some drugs, offset by access limitations or slower innovation at the margin.”

—Andrew F. Biernat, GBDS, CWCA

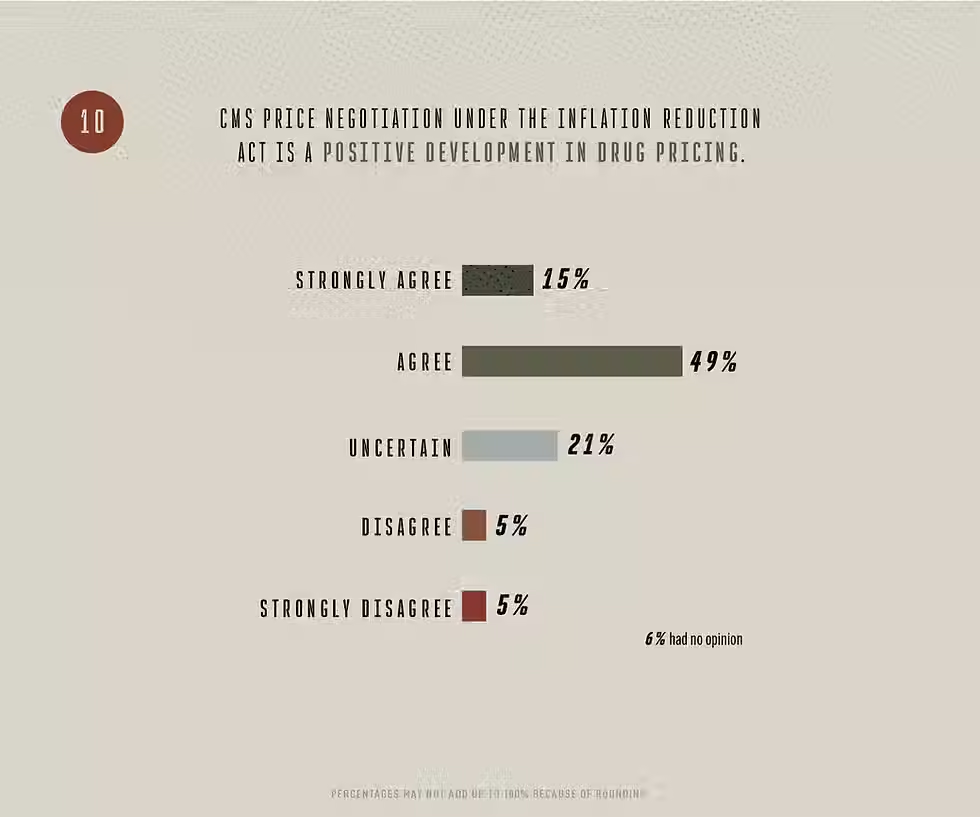

“On policy, while there is divergence in opinion and range of impact, industry is looking closely at the direct-to-patient and PBM reforms as key drivers in the near term. Respondents are mixed as to whether to attribute industry changes to the Trump administration policies but clearly recognize that pricing pressure is rising. Price negotiations under the IRA are viewed favorably as a factor in reducing drug prices but opinions are split on the impact on innovation… By a plurality, respondents do not think PBM reforms have gone far enough.”

—Luke Greenwalt, MBA

“The combination of federal PBM reform and federal drug price controls at the same time will be seen in history as changing managed care and the pharmaceutical industry. With PBMs forced to move away from revenue directly tied to drug prices, the microscope will be focused on the pharmaceutical industry to reduce costs; they won’t be able to blame PBMs anymore.”

—Jeff Casberg, RPh, M.S.

“The pharmaceutical industry will maintain its position as the best value in healthcare, reaching more patients than any other form of treatment. The role of pharmacists in the industry has a bright future in patient care, improving outcomes, research, managed care and many other nontraditional areas. When I speak to pharmacy students, they no longer envision only dispensing roles in their career futures. Use of AI in the pharmaceutical industry will also have a transformative impact on drug discovery, patient care, improving efficiency and reducing costs.”

—Jeff Casberg, RPh, M.S.

“Declining reimbursements, spread pricing and opaque rebate structure are compressing margins and threaten independent pharmacy viability (the three largest PBMs control approximately 70% of the U.S. market). Incentives are misaligned across payers, PBMs and manufacturers. Pharmacist and technician shortages are creating rising workloads and administrative burden is driving burnout rate. Moreover, underutilization in value-based care and fragmented data sharing hinder pharmacists’ ability to coordinate care, improve outcomes, and reduce total healthcare costs.”

—Andrew F. Biernat, GBDS, CWCA